How to Prepare for a Mortgage Loan Application

Prepare For A Mortgage Loan Application

After saving for a decent down payment that opens the doors to the lender’s office, every homebuyer gets excited when they are about to apply for a mortgage. But learning that not every lender is the same and that different products fit different needs makes it hard for GTA buyers to decide which mortgage package is the best for them regarding their specific financial situation. One dilemma buyers face is whether to go with a mortgage broker or their bank.

As a long-term customer, you may get some loyalty points and privileges if you go with your bank. In addition, the bank will have the data on your income and credit score ready, which means you don’t have to go through the bureaucratic ordeal of gathering all those documents. Banks are better equipped when it comes to other financial aspects as well, which can mean a lot to first-time buyers who are about to make the most significant investment in their life and need help to manage their finances. On the other hand, brokers are preferred because they offer more variety, i.e. presenting buyers with products from 40-50 lenders.

Check out listings in Brampton here.

A mortgage pre-approval makes it easier.

When it comes to pre-approval, it may not be mandatory, but it’s certainly helpful. Even if the pre-approved amount may not match the subsequent actual mortgage amount, it still gives you a price framework to work with. To avoid any misunderstandings, provide the lender with as accurate information as possible regarding your income, e.g., if you receive any bonuses, commissions or if you expect a promotion, etc.

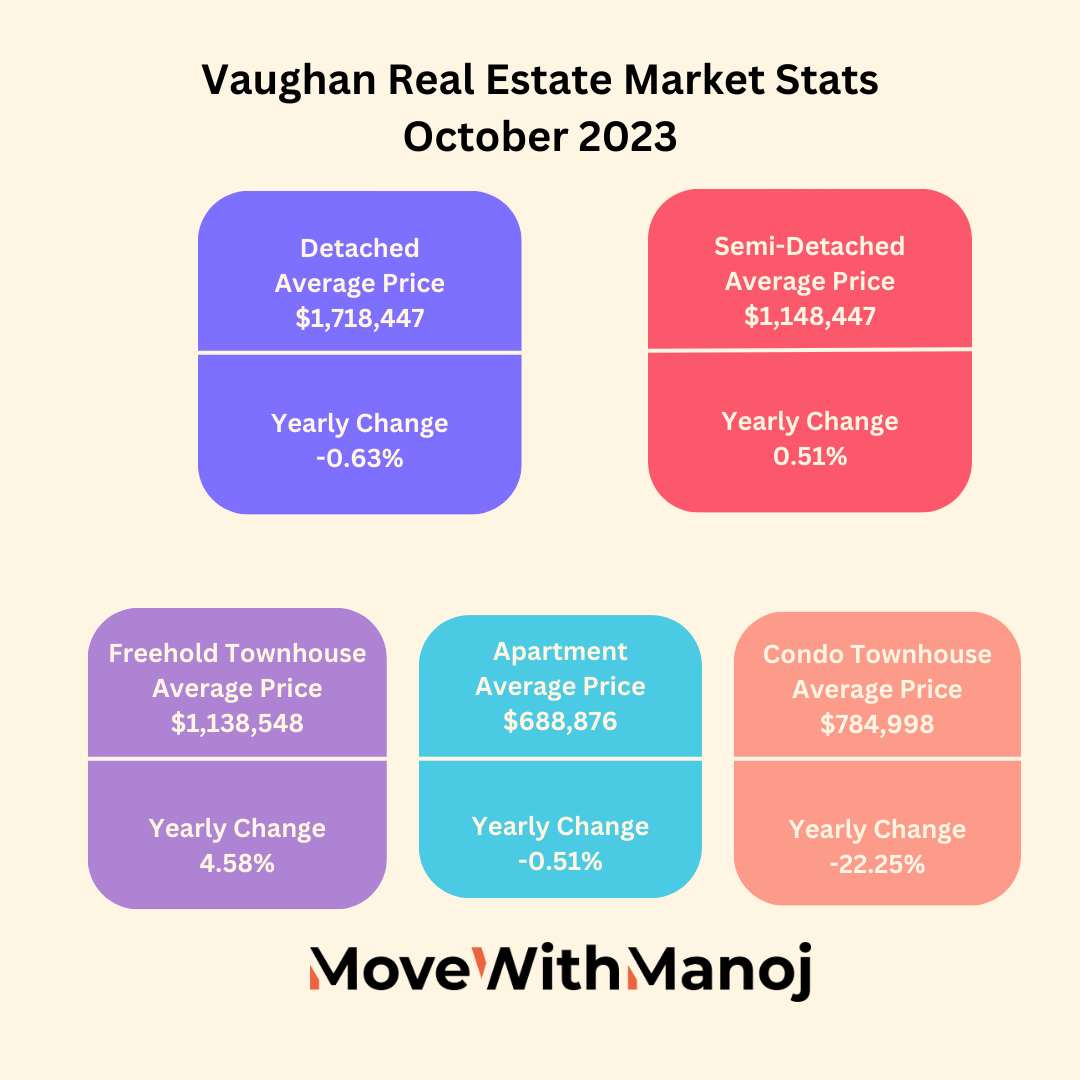

Check out listings in Vaughan here.

How much should the loan be

The lender will offer you the maximum you qualify for, but perhaps, you don’t want to max out the amount and go for a lower mortgage. Always leave some money for the RRSP, savings account or rainy days, etc. After all, today’s buyers are not ready to sacrifice perks like vacations or occasional splurges to pay off their homes faster. They would rather go with a lower mortgage or longer amortization to maintain a comfortable lifestyle. Make sure to precisely calculate how much you will have to give up in favour of the mortgage and if you are 100% OK with the monthly payments.

Check out listings in Mississauga here.

Rates, terms and amortization

Homebuyers usually don’t want to take unnecessary risks that are typically associated with the variable rate, e.g. they don’t want to depend on the volatile market conditions all the time. That’s why they prefer the fixed rate. It gives them a sense of stability, especially when mortgage rate increases are introduced every now and then. Some buyers may switch to variable ones (usually somewhat lower) in their third or fourth term when they gain more confidence.

Most homebuyers opt for a 5-year term, and that’s fine as long as they don’t forget to reflect on their needs when it’s time to renew the mortgage. On the other hand, maybe they have evolved over the years and need another lender who is a better fit for their existing situation.

Check out listings in Toronto here.

One of the throwbacks buyers have to consider is that their purchasing power was cut ever since the new mortgage stress tests were introduced. As a result, some buyers are now forced to take more extended amortization periods, e.g., 30 instead of 25 years, to get the desired mortgage amount. Even if this is the case, making occasional lump sum payments and allocating any extra income to the mortgage can quickly shrink the amortization by five years.

If you are looking to buy a home and would like to talk about finances and the GTA real estate market, contact Manoj Kukreja here.

{kind=link}

Comments